Each year, CERAWeek brings together the world’s most powerful energy leaders, but beyond the stage, it sparks a global media conversation that reveals which companies truly dominate the narrative around markets, policy, and the future of energy.

Here at CARMA, we analysed over 7,000 articles across 1,700 global outlets published from 1 March to 7 April through our insights platform. We analysed how energy companies are attempting to leverage geopolitical tensions to position themselves as both solutions to global challenges and symbols of progress in the public discourse.

Geopolitics is under the harsh media spotlight, and energy providers are crafting their messages accordingly.

Our data shows that CERAWeek was dominated by the coverage of hard energy realities. The theme ‘Energy Geopolitics’ accounts for 40% of article mentions, whilst ‘Oil Markets’ accounts for a further 28%. This far outweighs future-focused themes like AI and digitalisation (13%) and renewables (10%). This highlights how media attention remains firmly anchored in supply, security, and global power dynamics.

The audience is listening, but not passively.

The sentiment surrounding the event is predominantly neutral in online coverage (81%), reflecting fact-driven reporting, but drops notably when conversations shifted to social media (57%), as it is more opinion-led. While positive sentiment outweighs negative across both channels (17% online, 29% social), unsurprisingly, social media shows a more polarised response overall, with both higher positivity and a significantly larger share of negative sentiment (14% vs 2% online). This indicates a more engaged and reactive public discourse compared to traditional media.

The relatively strong positive sentiment across both traditional and social media suggests energy corporations are not only capturing attention but resonating with their audiences throughout the event and in subsequent media coverage. At a time of uncertainty and rising energy costs, our data shows that there is a clear appetite for authoritative voices and forward-looking perspectives. These events serve as more than just a platform for visibility; they can use it to actively enhance brand perception. Participating companies and leaders can position themselves as credible sources of solutions and stability in a complex global energy landscape.

Who led the conversation around CERAWeek?

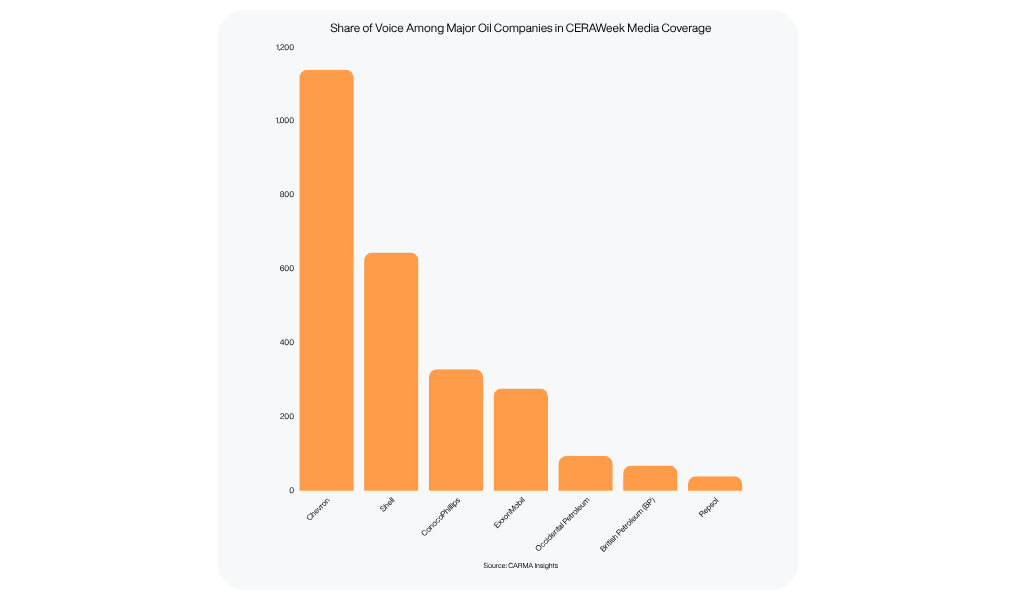

Focusing on the major oil companies present at CERAWeek provides a clear view of who truly dominated the conversation. Chevron emerged as the standout leader, accounting for 44% of total mentions among key players, well ahead of Shell (25%), ConocoPhillips (13%), and ExxonMobil (11%). Visibility is not evenly distributed either. A small number of companies, particularly those aligned with dominant themes around oil markets and supply constraints, are capturing the majority of all media attention.

Visibility follows relevance.

This concentration becomes even more compelling when viewed alongside search behaviour. Google News Trends* shows that attention closely correlates to global events. While Shell dominated search interest before 2025, reflecting its broader role across LNG, energy transition, and the global energy system, this shifted sharply in early 2026. A surge in interest around Chevron coincided with the US intervention in Venezuela and the capture of President Nicolás Maduro, a moment deeply tied to questions of oil access and global oil supply.

As the only major US oil company with a significant operational presence in Venezuela, Chevron quickly became central to media coverage surrounding the country’s vast reserves and potential reopening. This drove a sharp spike in visibility, a trend that continued into March and throughout CERAWeek. Rising geopolitical tensions, including the US/Iran conflict and risks to the Strait of Hormuz, further reinforced Chevron’s prominence. While these events elevated coverage for all major players, Chevron remained uniquely placed at the centre of the narrative due to its direct exposure to current supply disruptions.

A clear pattern emerges:

Chevron’s media visibility is highly event-driven, closely tied to global flashpoints that directly impact oil supply.

Short-term visibility and long-term perception are not always the same thing.

By contrast, Shell’s earlier dominance reflects a different type of narrative power. Its visibility is less tied to singular global developments and more to its role across LNG, energy transition, and a diversified energy portfolio. This distinction helps explain the shift from dominant Shell-led attention in 2025 to Chevron’s surge during this year’s CERAWeek. Demonstrating how media visibility is shaped not just by company presence, but by alignment with the most urgent challenges currently facing energy markets.

Interestingly, the difference is further evident in how each company framed its messaging during the event. As keynote discussions centred on supply disruptions and energy stability, Chevron tried to differentiate itself by focusing on the immediate need for continued investment and exploration. This broadly reinforces its focus on short-term, supply-driven messaging. Shell, meanwhile, aligned with this view but introduced a more forward-looking perspective, emphasising the growing importance of renewable energy within the future energy mix.

Shell’s discourse resonates more strongly with European markets, where energy security pressures, heightened by the Russia–Ukraine war and wider global instability, have accelerated the push toward diversification. Renewables are now being framed not only as a climate solution, but as a strategic response to reliance on imported energy.

These differences are clearly reflected in sentiment data. At a headline level, coverage of both companies remains overwhelmingly neutral, Chevron (93% neutral, 6% positive, 1% negative) and Shell (93% neutral, 5% positive, 2% negative), highlighting the largely fact-driven tone of coverage to come out of the event. However, a more nuanced picture emerges when isolating articles with unique mentions.

Here, Chevron’s coverage becomes significantly more polarised, with 53% negative sentiment and just 10% positive, suggesting that when discussed in isolation, it is more directly associated with geopolitical risk and supply disruption. In contrast, Shell maintains a more balanced and favourable profile, with 24% positive and 18% negative sentiment, alongside a higher neutral share (58%). Shell’s broader, transition-oriented approach helps buffer against negative sentiment, placing it not only within discussions of supply challenges and geopolitical tensions but also as a critical part of longer-term solutions.

Positive sentiment is driven by narratives of progress, not just participation.

Importantly, Chevron’s dominance should not be interpreted as purely reputational strength, but rather as a reflection of alignment with current audience priorities, namely oil supply, production growth, and price stability. This appetite for supply-focused solutions is evident across coverage of other companies operating in politically sensitive regions.

A strong example is Repsol. Despite lower overall visibility, it achieves a notably high 21% positive sentiment compared to just 3% negative. This is driven by its investment and expansion in Venezuela’s oil sector, a story that directly taps into the same supply-driven themes dominating CERAWeek.

What differentiates Repsol’s coverage, however, is its deeper connection to Venezuela’s evolving political environment. Following the capture of President Nicolás Maduro, power transitioned to acting President Delcy Rodríguez, whose leadership has been framed as more open to economic reform and external investment. As a result, energy investments are increasingly portrayed not just as commercial activity, but as part of a broader story of economic recovery and reintegration into global markets.

As a result, Repsol benefits from being framed within a more optimistic storyline. While Chevron’s coverage is closely tied to risk and uncertainty, Repsol’s is more often associated with opportunity, recovery, and future growth, explaining its stronger positive sentiment.

What energy brands should take away?

CERAWeek reveals a clear strategic media playbook:

- Relevance drives visibility – Align with real-time global developments to capture attention.

- Positioning drives perception – Connect to long-term energy solutions to build credibility.

- Narrative drives sentiment – Embed your brand within broader societal progress.

The brands that win within the media are not just present. They are strategically placed.

It starts with listening. Media intelligence gives you visibility into the conversations shaping your industry, what’s rising, what’s resonating, and where your brand fits.

But insight alone isn’t enough. The brands that lead are those that act on these signals early, consistently, and with clarity.

The Opportunity

CERAWeek makes one thing clear: The energy companies winning within the media and public landscape are not just responding to the story, they are embedding themselves at the centre of it.

At CARMA, we don’t just track coverage, we uncover the narratives driving visibility, sentiment, and influence, helping brands understand not just what is being said, but why it matters.

The question is:

Where does your brand sit in that narrative?